Roof Replacement Insurance Claim Guide: Navigate 2026 With Confidence

Severe storms are striking more often, leading to a surge in roof damage and costly repairs across neighborhoods. When disaster hits, navigating the roof replacement insurance claim process can feel overwhelming, especially if you are unsure where to begin.

Mistakes in handling a roof replacement insurance claim can result in denied coverage or unexpected expenses. That is why understanding each step is crucial.

This guide will walk you through what to do after roof damage, how to document and file claims, understanding your insurance policy, dealing with adjusters, and avoiding costly pitfalls. Take control of your outcome and secure the protection your property deserves.

Understanding Roof Replacement Insurance Coverage

Understanding your roof replacement insurance claim starts with knowing what type of policy you have. Most homeowners carry either an HO-3 or HO-5 policy, while business owners may have commercial property insurance. Each policy type offers different levels of protection for roof damage, which affects your eligibility for a roof replacement insurance claim.

Policies like HO-3 typically cover roof damage caused by specific perils, such as wind, hail, or fire. HO-5 policies offer broader protection and may cover more accidental losses. Commercial policies are tailored to business needs but share many of the same coverage principles. However, all policies have exclusions that impact your roof replacement insurance claim, such as wear and tear, poor maintenance, and pre-existing conditions.

Knowing what is covered is critical. Insurers usually pay for roof damage from sudden events, like storms or hail, but deny claims related to gradual deterioration. For example, if a Texas hailstorm damages your shingles, your roof replacement insurance claim is likely covered. If the roof fails due to age or neglect, the claim may be denied. According to the Roof repair insurance coverage resource, understanding these distinctions helps you avoid costly surprises when filing a roof replacement insurance claim.

Coverage is also determined by how your policy values your roof. Two main valuation methods are used: Actual Cash Value (ACV) and Replacement Cost Value (RCV). This difference can significantly affect your roof replacement insurance claim payout. Here is a simple comparison:

| Term | Definition | Impact on Claim |

|---|---|---|

| Actual Cash Value | Pays for replacement minus depreciation | Lower payout |

| Replacement Cost | Pays full cost to replace with new materials | Higher payout |

If your policy uses ACV, the insurer subtracts depreciation based on age and condition, so your roof replacement insurance claim may cover only a portion of the costs. RCV policies pay the full price to restore your roof to its original condition, minus your deductible.

Deductibles are another key factor. The average wind and hail deductible in Texas ranges from 1% to 2% of the insured value, often totaling several thousand dollars. Nationally, roof claim deductibles are rising as insurers respond to increased storm frequency and higher claim costs. According to recent industry reports, roof claims in the U.S. exceeded $30 billion in 2024, with wind and hail responsible for the majority.

To maximize your roof replacement insurance claim, review your policy’s declarations page and any endorsements. This section lists your specific coverage, limits, and deductibles. Pay attention to key terms and clauses like:

- Depreciation: Reduction in payout for older roofs

- Matching: Requirement to match materials for uniform appearance

- Code Upgrades: Coverage for bringing repairs up to current building codes

Some policies may limit or exclude coverage for roofs over a certain age, or require specific materials to qualify for replacement cost coverage. Insurers have tightened these requirements recently, especially in storm-prone areas, making it vital to read every detail related to your roof replacement insurance claim.

Staying informed about your policy terms and recent trends helps you avoid surprises and ensures your roof replacement insurance claim is as strong as possible. Always document your roof’s condition, keep maintenance records, and consult an expert if you need help interpreting your coverage.

Recognizing Roof Damage and When to File a Claim

Assessing roof damage after a storm is critical. Quick action can make the difference between a smooth roof replacement insurance claim and a stressful, costly process. Knowing what damage your policy covers, when to file a claim, and how to document everything will help you avoid common setbacks.

Types of Roof Damage Covered by Insurance

Most roof replacement insurance claim payouts result from severe weather. Standard policies typically cover sudden, accidental events like:

- Hailstorms

- High winds

- Lightning or fire

These are recognized by insurers as "covered perils." For example, after a major Texas hailstorm, claim volumes can spike by over 50%, reflecting just how frequently such events lead to roof replacement insurance claim filings. In fact, severe weather events account for nearly 80% of all roof claims nationwide.

However, not all roof issues qualify. Insurers often exclude gradual wear, poor maintenance, or pre-existing problems. Recognizing the difference is essential—missing shingles after a windstorm are likely covered, but moss growth or old leaks typically are not.

Look for dents, bruising, torn shingles, or visible impact marks after storms. Compare these to signs of aging, like curling or general granule loss, which are usually maintenance concerns. For more real-world examples and resources on storm-related claims, visit storm damage insurance claims.

Timely action is vital: insurers expect prompt notification after major weather events to validate your roof replacement insurance claim.

When to File a Claim (and When Not To)

Not every roof issue requires a roof replacement insurance claim. Before contacting your insurer, evaluate the extent and cause of the damage. If repairs are minor and cost less than your deductible, paying out-of-pocket may be wiser to avoid premium hikes or potential non-renewal.

Unnecessary claims can backfire. Insurers track your claim history, and excessive or unjustified filings may lead to higher rates or denied future coverage. Always check your state’s deadline for filing claims—Texas, for example, often requires claims to be submitted within one to two years of the event.

Claims filed late or without enough proof are often denied. For example, a homeowner who waited months after a hailstorm and lacked clear documentation saw their roof replacement insurance claim rejected. Ensure you act promptly and keep detailed records to protect your rights.

Documenting Damage for Your Claim

Thorough documentation is crucial for a successful roof replacement insurance claim. Start by taking clear, timestamped photos and videos of all visible damage. Capture wide shots of the roof and close-ups of specific issues.

Keep weather alerts, news articles, and repair estimates as backup evidence. Maintain inspection reports from both independent contractors and your insurer. Detailed records help demonstrate the damage was storm-related and not due to neglect.

One Texas homeowner’s careful documentation—photos, news clippings, and contractor reports—led to a fast, full payout on their roof replacement insurance claim when adjusters questioned the cause of damage. The right evidence can make all the difference.

Step-by-Step Roof Replacement Insurance Claim Process

Navigating the roof replacement insurance claim process can feel overwhelming, but breaking it into clear, actionable steps makes all the difference. A systematic approach maximizes your claim, controls costs, and reduces stress. Let’s walk through each step, highlighting what you need to do, when, and why it matters.

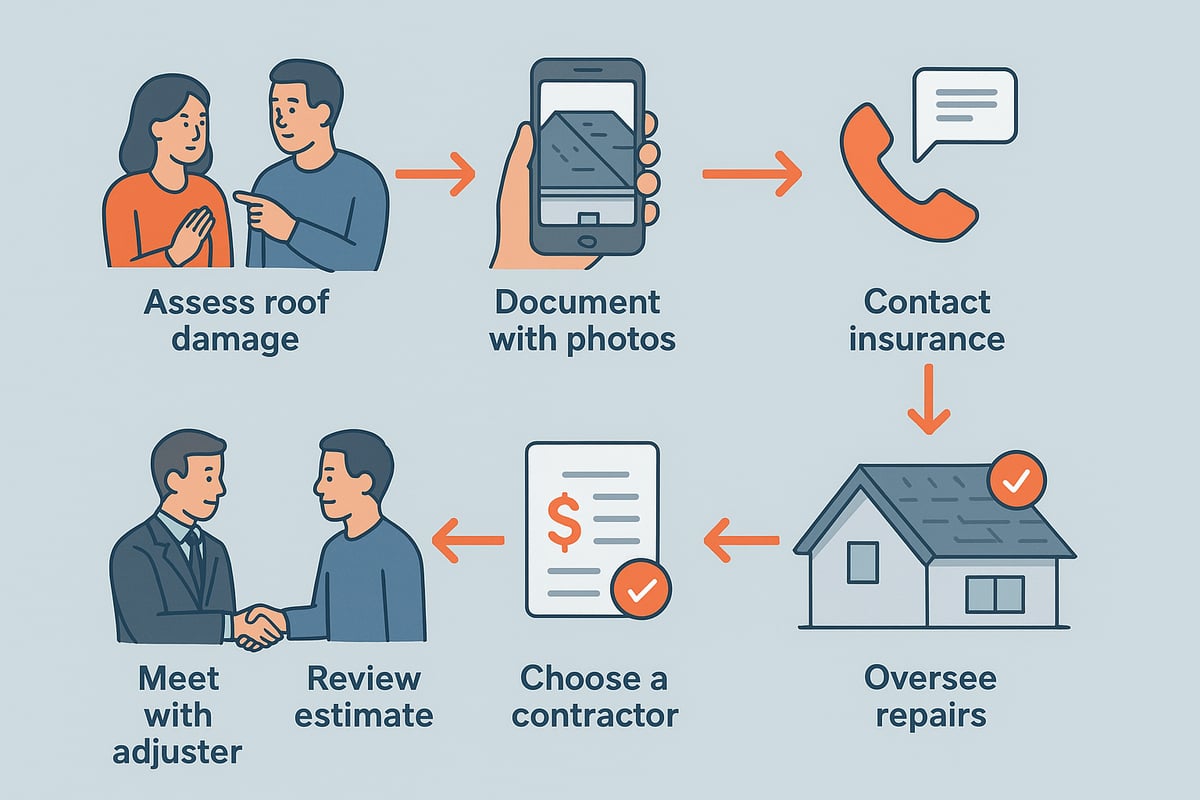

Step 1: Inspect and Document Damage

Your first priority after any storm or incident is safety. Avoid climbing onto the roof yourself. Instead, inspect from the ground using binoculars or hire a qualified roofing professional.

Document all visible damage with clear, timestamped photos and videos. Capture shingles in the yard, dents, granule loss, or exposed underlayment. Record the date, time, and details about the weather event.

Post-Storm Roof Inspection Checklist:

- Photograph all affected areas from multiple angles

- Note down interior water stains or leaks

- Save news reports or weather alerts for proof of storm

Thorough documentation is essential for a successful roof replacement insurance claim.

Step 2: Notify Your Insurance Carrier Promptly

Contact your insurance provider as soon as possible. Use the claims phone line, online portal, or your agent, whichever is most convenient.

Have your policy number, details of the event, and initial documentation ready. Request a claim number and written confirmation of your claim initiation.

Insurers often require notification within a specific timeframe after damage occurs. For example, after a major storm, most policies require that you start your roof replacement insurance claim within days to weeks. Acting quickly helps prevent delays or denials.

Step 3: Schedule a Professional Roof Inspection

Arrange for a reputable roofing contractor to conduct a detailed inspection. Some insurers recommend preferred vendors, but you are entitled to hire an independent, licensed professional.

A comprehensive inspection report should include photos, diagrams, and a written assessment of both visible and hidden damage. This documentation can uncover issues an adjuster might miss, strengthening your roof replacement insurance claim.

For example, a professional may identify underlying structural or water damage that is not immediately obvious, ensuring your claim reflects the full scope of necessary repairs.

Step 4: Meet With the Insurance Adjuster

Your insurer will assign an adjuster to inspect your property. Be present during the appointment. Provide all documentation, including your contractor’s report and photographs.

It is wise to have your roofing contractor or a public adjuster attend. They can point out less obvious damage and advocate for a comprehensive assessment.

If the adjuster misses secondary issues, such as flashing or vent damage, bring it to their attention immediately. This step is critical for an accurate roof replacement insurance claim.

Step 5: Review the Insurance Estimate and Scope of Work

Once the adjuster completes their inspection, you will receive an estimate outlining the scope of repairs, line items, actual cash value, replacement cost, and depreciation.

Review the estimate closely. If items are missing or the proposed payout is too low, request a re-inspection or submit a supplement. Your contractor can help identify discrepancies.

For instance, a supplement may increase your payout significantly if additional damage is documented. Understanding the details ensures your roof replacement insurance claim fully covers restoration.

Step 6: Choose a Reputable Roofing Contractor

Selecting the right contractor is essential. Vet candidates for licensing, insurance, and local reputation. Avoid storm chasers or out-of-state operators who may disappear after the job.

Contractor Vetting Tips:

- Verify credentials and insurance coverage

- Ask for local references and completed project photos

- Demand a detailed contract outlining materials, timelines, and warranties

A homeowner once hired an unlicensed contractor and faced costly repairs later. Protect your roof replacement insurance claim by choosing wisely.

Step 7: Overseeing Repairs and Finalizing Your Claim

Monitor the repair process to ensure quality workmanship and job site safety. Keep records of all invoices, receipts, and completion photos.

Submit final paperwork to your insurer for any recoverable depreciation payments. The insurer may require proof of completed work before releasing the last funds.

Missing documentation can delay payments, so keep everything organized. A smooth process ensures your roof replacement insurance claim pays out fully and promptly.

For a comprehensive breakdown of these steps and additional guidance, consider reviewing the Roofing insurance claims process for deeper insights tailored to your situation.

Navigating Insurance Adjusters, Disputes, and Negotiations

When you file a roof replacement insurance claim, the insurance adjuster is your first point of contact for assessing damage and estimating costs. The adjuster inspects your roof, reviews documentation, and determines what your policy covers. However, adjusters work for the insurer, not you, so their assessment may not always align with your expectations or needs.

Being prepared for adjuster visits matters. Adjusters can only approve damages clearly tied to covered events and documented properly. They often cannot authorize code upgrades or repairs for pre-existing issues. If you feel your roof replacement insurance claim is not being fairly evaluated, it is important to understand your rights and options.

Common Reasons for Underpaid or Denied Claims

Many roof replacement insurance claim denials or underpayments stem from a few recurring issues. The most frequent are:

| Reason | Description |

|---|---|

| Pre-existing damage | Insurer claims issue existed before the event |

| Cosmetic-only damage | Insurer says damage is not functional |

| Late filing | Claim submitted past the policy deadline |

| Insufficient documentation | Lack of photos, reports, or weather evidence |

| Maintenance neglect | Insurer finds poor upkeep led to the problem |

Insurers are also increasingly citing exclusions and depreciation, especially for older roofs. A lack of detailed records or a missed deadline can result in a denied roof replacement insurance claim, even if the damage is legitimate. Reviewing your policy and understanding these pitfalls is key to successful claims.

Challenging a Low Estimate: Supplements, Opinions, and Public Adjusters

If your roof replacement insurance claim is underpaid or denied, you are not out of options. Start by requesting a detailed explanation of the adjuster’s estimate. Compare their scope of work with your contractor’s inspection report. Discrepancies, such as missed components or undervalued repairs, are grounds for a supplement request.

You may benefit from bringing in a public adjuster or an independent roofing expert to reassess the damage. Their detailed reports often highlight issues missed by the insurer’s adjuster. For more on effective documentation and claim strategies, review the Guide to Roof Damage Insurance Claims, which outlines each step with practical advice.

Documentation and Negotiation Strategies

Strong documentation is your best defense in a roof replacement insurance claim dispute. Keep all photos, repair estimates, inspection reports, and communication logs organized. Written records of every interaction with your insurer or adjuster can be crucial if you need to escalate your claim.

Consider this real-world example: A homeowner in Texas initially received a denial due to “insufficient evidence.” By submitting additional photos, news reports of the storm, and a contractor’s letter, they secured a $15,000 supplement on their roof replacement insurance claim. Persistence and thorough records often make the difference.

Mediation, Appraisal, and Legal Recourse

If negotiations stall, most policies allow you to pursue mediation, appraisal, or even legal action. Mediation involves a neutral third party guiding both sides toward a compromise. The appraisal process lets each party hire an appraiser, with a neutral umpire resolving disagreements. Legal action is typically the last resort if all other methods fail.

According to the U.S. Roofing Realities Trend Report, nearly 25% of roof replacement insurance claim payouts increase after professional negotiation or dispute processes. Knowing your options gives you leverage.

Importance of Communication Records and Written Agreements

Throughout your roof replacement insurance claim, keep detailed records of every phone call, email, and document exchange. Always request written confirmation of agreements, changes to estimates, or claim decisions. These records protect your interests if disputes arise later.

Clear, organized communication not only streamlines the process but also strengthens your position if you need to contest an adjuster’s findings or escalate your claim. By staying proactive and informed, you can maximize your coverage and ensure a fair resolution.

Avoiding Common Pitfalls and Maximizing Your Claim

Homeowners and property managers often face challenges during the roof replacement insurance claim process. Missteps can result in denied claims, reduced payouts, or unnecessary stress. By understanding common pitfalls and learning strategies to maximize your claim, you can secure the coverage you deserve and avoid costly mistakes.

Mistakes That Can Jeopardize Your Claim

Even small errors during the roof replacement insurance claim process can have major consequences. Some of the most frequent mistakes include:

- Failing to notify your insurer promptly. Delays can violate policy terms and result in denied coverage.

- Incomplete documentation. Missing photos, weather records, or repair estimates weaken your claim.

- Accepting the first offer without review. Insurers may underestimate repair costs, so always scrutinize the initial settlement.

- Hiring unlicensed or out-of-state contractors. This can void warranties and affect claim approval.

- Neglecting maintenance records. Insurers often deny claims if lack of upkeep is suspected.

For example, a homeowner in Texas had a roof replacement insurance claim denied because they could not provide records of annual inspections. This underscores the importance of routine documentation. Another common issue is missing state filing deadlines. In Texas, you typically have one to two years to file a claim after the event, but late submissions are a leading cause of denials.

Table: Common Pitfalls vs. Solutions

| Pitfall | Solution |

|---|---|

| Late claim notification | Notify insurer immediately |

| Poor documentation | Take clear, timestamped photos/videos |

| Accepting low initial offer | Request review or supplement |

| Hiring unlicensed contractors | Verify credentials and local reputation |

| Missing maintenance records | Keep yearly inspection reports |

By staying proactive and organized, you can prevent these costly errors and improve your roof replacement insurance claim outcome.

Tips to Maximize Your Roof Replacement Insurance Claim

Maximizing your roof replacement insurance claim requires more than submitting paperwork. Consider these proven strategies:

- Schedule annual roof inspections. This creates a record of maintenance and helps identify issues early.

- Upgrade to impact-resistant materials. Some policies offer better terms for improved roofing products.

- Use a local, reputable contractor. Local experts understand insurance requirements and can help document damage accurately.

- Maintain detailed communication records. Save every email, letter, and note related to your claim.

- Understand your policy’s specifics. Review depreciation, matching, and code upgrade clauses before filing.

A Texas homeowner recently maximized their roof replacement insurance claim by providing thorough documentation and working closely with an experienced contractor. Their proactive approach led to a full payout for storm-related damage.

For a more detailed step-by-step approach, consider reviewing this Roof replacement guide, which complements the tips provided here and helps you avoid common mistakes from the start.

Staying Informed About Policy Changes and Local Regulations

Insurance policies and state laws are constantly evolving. Staying updated on these changes is crucial for anyone filing a roof replacement insurance claim.

Recent Texas legislation has introduced stricter requirements for roof age and materials. Insurers may exclude older roofs or impose higher deductibles. Always read policy updates and consult with your agent about new code compliance rules.

Resources such as local roofing associations and state insurance departments can help you stay ahead of regulatory changes. By staying informed, you protect your investment and ensure your roof replacement insurance claim is not affected by unexpected policy shifts.

You’ve just learned how crucial it is to navigate the roof replacement insurance claim process with the right support—especially when every detail and deadline matters. If you’re unsure where to start, or want an expert on your side to help with documentation, negotiations, and maximizing your claim, you don’t have to go it alone. The Texcore Construction team specializes in guiding Fort Worth property owners through every step, providing clarity, transparency, and peace of mind from inspection to final approval. Let’s make your insurance claim as smooth and successful as possible—Talk to Our Insurance Claims Team Today.